Bonds for Retirement: A Safe and Reliable Investment

Embark on an exciting journey as we explore the world of bonds - a hidden treasure in the realm of retirement investments. This guide will illuminate the path to a safe and reliable financial future. Prepare to be amazed!

Reasons to Own Bonds for Your Retirement

Governments, towns, and corporations issue bonds as a means of raising finance. Purchasing a bond is simply lending money to the issuer in return for regular interest payments and the maturity payment of the bond's face value. Bonds are very beneficial in a retirement strategy for the following reasons:

- Stable Income: Bonds offer coupon payments, or periodic interest payments, that can be a dependable source of income in retirement. Particularly beneficial to retirees who must pay living expenses without depending on more erratic stock markets is this steady stream of income.

- Capital Preservation: Given that they provide a fixed return and the principal is returned upon maturity, bonds are typically regarded as safer investments than stocks. They are therefore a desirable choice for seniors seeking a moderate return on their capital.

- Diversification: Bonds can help diversify your investments and lower the total risk of your retirement portfolio. In addition to acting as a hedge against market downturns and aiding in portfolio stabilization, bonds frequently perform differently from stocks.

- Inflation Protection: Although conventional bonds may be susceptible to inflation, some bond kinds, including Treasury Inflation-Protected Securities (TIPS), are made to shield your money from inflation's deteriorating impacts. They are therefore a crucial instrument for preserving purchasing power in retirement.

Bonds are an important component of a retirement portfolio because they provide a certain level of stability that is necessary for those who are dependent on their savings for income rather than wealth accumulation.

Different Types of Retirement Bonds

Retirees can choose from a variety of bond types when assembling their financial portfolios. Since every kind of bond has unique risk and return characteristics, it's critical to comprehend how each fits into your entire retirement plan.U.S. Treasury Bonds

- Treasury Bills (T-Bills): Short-term securities with a one-year maturity or less. The interest earned is represented by the difference between the purchase price and face value, which is discounted when they are sold.

- Treasury Notes (T-Notes): Medium-term securities with maturities varying from two to ten years. T-Notes reimburse the principal at maturity and pay interest every six months.

- Treasury Bonds (T-Bonds): Long-term investments with maturities of 20 or 30 years. T-Bonds refund the principal at maturity and pay interest semiannually, just like T-Notes.

- Treasury Inflation-Protected Securities (TIPS): These securities are intended to guard against inflation by modifying the principal amount in response to fluctuations in the Consumer Price Index (CPI). TIPS are a useful instrument for maintaining purchasing power in retirement because interest is paid semiannually on the adjusted principal.

Municipal Bonds

- General Obligation Bonds: These bonds are regarded as extremely safe, even though they might have a somewhat lower yield than revenue bonds because they are backed by the issuing municipality's whole taxing capacity.

- Revenue Bonds: Backed by the money received from a particular project (such as a utility or toll road). Revenue bonds pose a somewhat higher risk than general obligation bonds because their yields are dependent on the project's success.

Corporate Bonds

Companies issue corporate bonds to raise money for various purposes such as expansion, business operations, or other projects. Generally speaking, these bonds have greater yields than U.S. Treasury and municipal bonds, which represent the increased risk involved in making a loan to a business. Different corporate bond grades exist:

-

Investment-Grade Bonds: Issued by businesses that have excellent credit ratings (BBB or above from Standard & Poor's, or Baa3 or higher from Moody's). Because of their lower risk, these bonds are a good option for conservative investors looking for higher yields than government bonds.

-

High-Yield Bonds (Junk Bonds): These bonds, which come with a higher default risk, are issued by corporations with poor credit ratings. Risk-averse retirees are often advised against investing in high-yield bonds due to their higher volatility.

Adding corporate bonds to a retirement portfolio can be beneficial, particularly for individuals looking to increase their income. However, controlling the risks related to corporate bonds requires careful selection and diversification.

Bond ETFs and Funds

ETFs and bond funds provide a simple option for retirees who want to invest in bonds in a diversified manner. These funds combine the capital of several investors to buy a variety of bonds. ETFs and bond funds come in a variety of forms:

-

Government Bond Funds: These funds mainly focus on U.S. Treasury and government agency bonds, providing retirees looking to preserve their savings and earn income with minimal risk.

-

Municipal Bond Funds: Focus on tax-exempt municipal bonds and offer tax-efficient income to investors in higher tax brackets.

-

Corporate Bond Funds: Invest in a diverse portfolio of corporate bonds, which can generate higher yields at different risk levels based on the bonds' credit quality.

-

High-Yield Bond Funds: Concentrate on corporate bonds with lower ratings, which have greater yields but are riskier. Retirees who can tolerate more risk should invest in these funds.

For retirees who wish exposure to bonds without having to manage individual bond investments, bond funds and exchange-traded funds (ETFs) offer professional management and diversification.

Tips for Including Bonds in Your Retirement Investment Portfolio

Creating a plan for adding bonds to your retirement portfolio is the next step after learning about the many kinds of bonds that are out there. Here are some crucial tactics to think about:

Laddering

Buying bonds with varying maturities is a tactic known as bond laddering. You might purchase bonds with maturities of 2, 4, 6, 8, and 10 years, for instance. You can reinvest the capital into a new bond at the long end of the ladder as each bond expires. This strategy has numerous advantages:

-

Income Stability: The bonds' staggered maturities provide a consistent flow of income since you'll receive principle repayments from maturing bonds along with regular interest payments.

-

Interest Rate Risk Mitigation: Laddering helps reduce interest rate risk since it keeps you from being committed to a single interest rate for an extended amount of time. Bonds that are about to mature can be reinvested at higher returns if interest rates rise.

-

Liquidity: You can access your capital at regular intervals without needing to sell bonds before they mature thanks to the regular maturity dates.

A cautious approach that can manage interest rate risk and give retirees a steady income stream is bond laddering.

Allocation Based on Risk Tolerance

The proportion of bonds in your portfolio should be determined in large part by your tolerance for risk. In general, the percentage of bonds in your portfolio will increase with your proximity to retirement or level of risk aversion. The "100 minus age" rule is a popular guideline that states you should allocate a certain amount of your portfolio to stocks and the remaining portion to bonds. You calculate this by subtracting your age from 100. A 65-year-old retiree, for instance, might have 65% of their portfolio in bonds and 35% in stocks.

Nonetheless, bear in mind that this is only a general guideline, and specific factors such as your overall financial status, retirement objectives, and risk tolerance should be taken into account when deciding how much bond to allocate.

Rebalancing Your Portfolio

It's critical to periodically rebalance your portfolio as you approach retirement to make sure it stays in line with your financial objectives and risk tolerance. Rebalancing is making portfolio adjustments to keep your intended asset allocation. To restore your desired allocation, you might need to sell some stocks and reinvest the proceeds in bonds if, for instance, a notable stock market rise leads the stock component of your portfolio to grow excessively.

Continuous rebalancing guarantees that your portfolio is suitably diversified during retirement and helps control risk.

Consider Inflation-Linked Bonds

For retirees, inflation is a major worry because over time, it can reduce the purchasing power of your fixed-income investments. Think about including inflation-linked bonds, like Treasury Inflation-Protected Securities (TIPS), in your portfolio as a means of guarding against inflation. To ensure your investment keeps up with inflation, TIPS adjust their principal value based on changes in the Consumer Price Index (CPI).

Adding TIPS to your bond portfolio can help you stay worry-free and preserve your purchasing power in retirement.

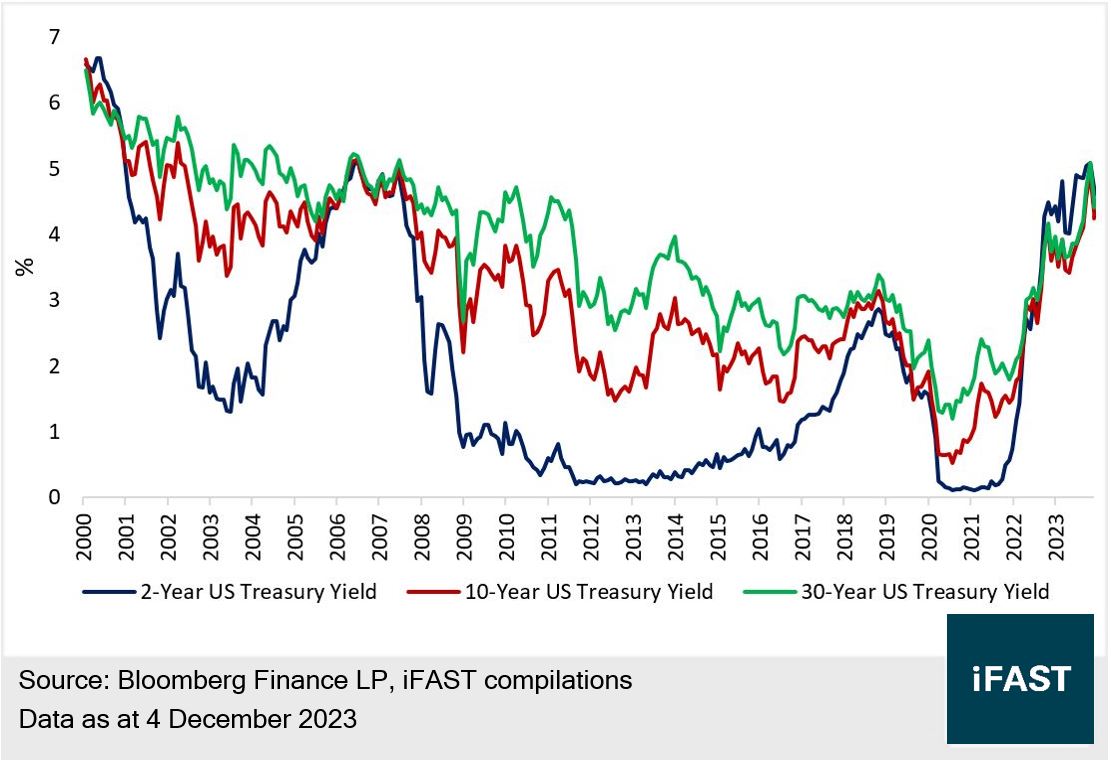

The Present U.S. Bond Market Conditions

The U.S. market environment in 2024 presents a range of opportunities and challenges for bond investors. Here’s how the state of the economy is impacting bond investments:Interest Rates

Inflation

Market Volatility

Credit Risk

Result

Bonds continue to be an essential part of a balanced retirement strategy because they provide diversification, stability, and income. Bonds provide retirees a secure and dependable investment choice in the current volatile U.S. market climate, which is marked by rising interest rates and inflation. You may build a bond portfolio that fits your risk tolerance and financial objectives by being aware of the many bond kinds that are out there, using techniques like laddering and rebalancing, and taking inflation-linked bonds into consideration.

Like with any investment, it's critical to keep up with market developments and modify your plan as necessary. Collaborating with a financial counselor may additionally assist you in managing the intricacies of bond investing and guarantee that your retirement fund is suitably positioned to furnish a safe and cozy retirement.

You May Also Like: