Umbrella Insurance: A Comprehensive Guide

As the U.S. economy continues to face various challenges, individuals and families must prioritize protecting their financial assets. One effective way to achieve this protection is through umbrella insurance. In this comprehensive guide, we will explore the concept of umbrella insurance, its importance in today's economic climate, and how it can provide a crucial safety net against unforeseen financial liabilities.

The Current U.S. Economic Environment

Overview of the Economic Landscape

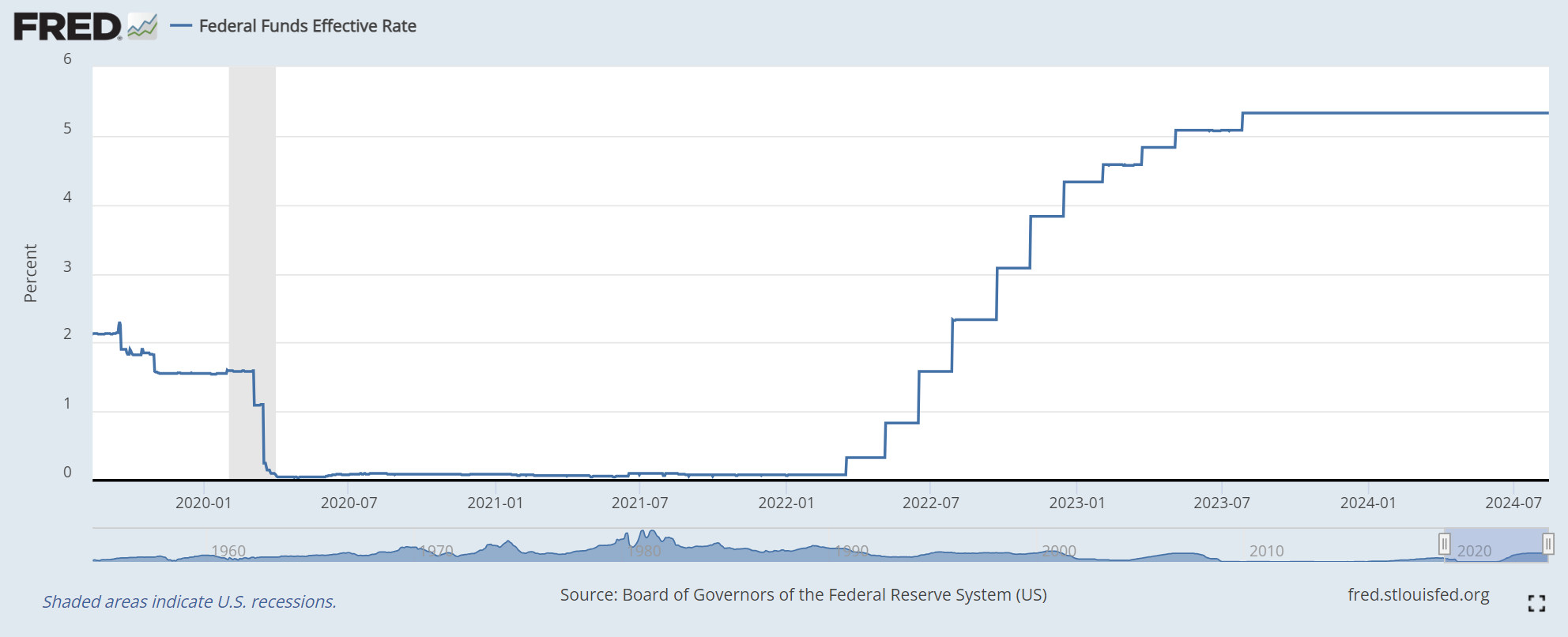

The U.S. economy is currently navigating a complex landscape characterized by inflation, fluctuating interest rates, and varying levels of unemployment. The post-pandemic recovery has been uneven, leading to uncertainty in both the stock market and real estate sectors. Additionally, legal and medical costs continue to rise, putting pressure on individuals who may face lawsuits or significant liability claims.

Influence on Personal Finance Decisions

In such an unpredictable economic environment, consumers are becoming more cautious with their financial decisions. The need for comprehensive risk management strategies has never been greater, and this is where umbrella insurance becomes essential. With the potential for high legal costs and the risk of depleting savings or losing assets, umbrella insurance offers peace of mind by providing coverage beyond standard policies.

Asset Protection During Economic Uncertainty

Inflation erodes the value of money over time, making it more difficult to rebuild savings or recover from financial setbacks. Furthermore, economic instability increases the likelihood of litigation, especially in cases involving property disputes, accidents, or professional liabilities. Umbrella insurance acts as a safeguard, ensuring that individuals are protected from catastrophic financial losses that could arise during economic downturns.

What is Umbrella Insurance?

Detailed Explanation of Umbrella Insurance

Umbrella insurance is a type of personal liability insurance that provides coverage beyond the limits of your existing policies, such as auto or homeowners insurance. It covers not only the policyholder but also their family members and even legal fees incurred during lawsuits. This coverage is especially valuable in situations where standard insurance policies may fall short, offering additional protection against a wide range of liability risks.

Differences Between Umbrella Insurance and Other Types of Insurance

While standard insurance policies, like auto or home insurance, provide coverage for specific incidents up to a certain limit, umbrella insurance extends this coverage further. It kicks in when the liability limits of these primary policies are exhausted. For example, if you are involved in a car accident and the damages exceed your auto insurance coverage, your umbrella insurance policy can cover the remaining costs.

Scenarios Where Umbrella Insurance is Applicable

Umbrella insurance is beneficial in various scenarios, including:

- Auto Accidents: If you cause a severe car accident resulting in multiple injuries, the costs can quickly exceed your auto insurance coverage. Umbrella insurance can cover the excess amount.

- Property Incidents: If someone is injured on your property and the medical bills and legal fees surpass your homeowners insurance limits, umbrella insurance can provide the additional needed coverage.

- Personal Lawsuits: If you are sued for defamation, libel, or slander, which are typically not covered by standard insurance policies, umbrella insurance can cover legal fees and settlements.

Why Umbrella Insurance is Crucial in the Current Economy

Impact of Rising Lawsuits and Legal Costs

The current economic environment has seen a rise in the number of lawsuits, driven by economic stress and the increasing complexity of legal disputes. Legal costs are also on the rise, making it essential for individuals to have sufficient liability coverage. Without umbrella insurance, a single lawsuit could lead to significant financial hardship, especially if the costs exceed the coverage limits of standard insurance policies.

The Role of Umbrella Insurance in Protecting Against Large Financial Losses

Umbrella insurance is designed to protect against large, potentially devastating financial losses. In a litigious society like the United States, where even minor incidents can lead to expensive lawsuits, having an umbrella policy provides an additional layer of security. This coverage can be the difference between maintaining financial stability and facing bankruptcy due to unforeseen legal liabilities.

How Inflation and Economic Instability Increase Liability Risks

Inflation and economic instability amplify the risks associated with liability claims. As the cost of living rises, so do the potential damages awarded in lawsuits. Medical expenses, property repairs, and legal fees can quickly escalate, outpacing the coverage provided by standard insurance policies. Umbrella insurance helps mitigate these risks by offering higher coverage limits and broader protection.

Benefits of Umbrella Insurance

Extensive Coverage Beyond Standard Policies

One of the primary benefits of umbrella insurance is the extensive coverage it provides beyond standard policies. This coverage includes not only bodily injury and property damage but also personal liability issues such as defamation, false arrest, and invasion of privacy. By covering a wide range of scenarios, umbrella insurance ensures that you are protected against various risks that could otherwise lead to financial ruin.

Coverage of Legal Fees and Settlements

Legal fees can be exorbitant, especially in complex cases involving multiple parties or prolonged litigation. Umbrella insurance covers these legal expenses, which can be a significant relief for individuals facing lawsuits. Additionally, if a settlement is reached or a judgment is awarded against you, the policy can cover these costs, ensuring that your personal assets are not depleted.

Peace of Mind for Individuals with Substantial Assets

For individuals with substantial assets, such as real estate, investments, or businesses, umbrella insurance offers peace of mind. Knowing that your wealth is protected from unforeseen liabilities allows you to focus on other important aspects of life, such as family, career, and personal goals. The security provided by umbrella insurance is invaluable, especially in an unpredictable economic environment.

Challenges and Considerations

Potential Drawbacks of Umbrella Insurance

While umbrella insurance offers significant benefits, there are also potential drawbacks to consider. For example, not all risks are covered by umbrella policies, and certain exclusions may apply. Additionally, the cost of umbrella insurance, though generally affordable, can vary depending on factors such as your location, assets, and the level of coverage you require.

Cost vs. Benefit Analysis in the Current Economic Context

In the current economic context, it is essential to conduct a cost vs. benefit analysis when considering umbrella insurance. While the premium costs are relatively low compared to the coverage provided, individuals must assess their risk exposure and determine if umbrella insurance is a necessary investment. For those with significant assets or higher risk profiles, the benefits of umbrella insurance often outweigh the costs.

Consideration of Personal Risk Factors and Assets

When deciding whether to purchase umbrella insurance, it is important to consider your personal risk factors and assets. Individuals with higher exposure to liability risks, such as property owners, business owners, or those with a public presence, may find umbrella insurance particularly valuable. Assessing your assets, lifestyle, and potential liabilities will help you make an informed decision about whether umbrella insurance is right for you.

Who Should Consider Umbrella Insurance?

High-Net-Worth Individuals

High-net-worth individuals, who have significant financial assets and investments, should strongly consider umbrella insurance. Their wealth makes them more susceptible to lawsuits and larger liability claims, and umbrella insurance provides the additional coverage needed to protect these assets from being targeted in legal actions.

Small Business Owners

Small business owners often face a variety of liability risks, from employee-related incidents to customer injuries on business premises. Umbrella insurance can offer protection beyond the limits of commercial liability policies, safeguarding personal and business assets against costly lawsuits.

Professionals in High-Risk Occupations

Professionals in high-risk occupations, such as doctors, lawyers, or architects, may face malpractice claims or other professional liability issues. Umbrella insurance provides an extra layer of protection in these situations, covering legal fees and damages that exceed the limits of professional liability insurance.

Property Owners and Landlords

Property owners and landlords should also consider umbrella insurance, especially if they own multiple properties or rental units. The risks associated with property ownership, such as tenant injuries or property damage, can lead to substantial liability claims. Umbrella insurance helps protect personal assets from these risks.

How to Choose the Right Umbrella Insurance Policy

Factors to Consider When Selecting a Policy

When choosing an umbrella insurance policy, several factors should be considered:

- Coverage Limits: Ensure that the policy provides adequate coverage based on your assets and potential liability risks.

- Exclusions: Review the policy exclusions to understand what is not covered and whether additional coverage is needed.

- Premium Costs: Compare premium costs from different insurers to find a policy that offers the best value for your needs.

- Insurer Reputation: Choose an insurer with a strong reputation for customer service and claims handling.

Understanding Policy Limits and Exclusions

Policy limits and exclusions are critical aspects of umbrella insurance that must be understood before purchasing a policy. The coverage limits should be sufficient to protect your assets, while the exclusions should be carefully reviewed to ensure that potential risks are not overlooked. In some cases, additional coverage may be needed to address specific risks not covered by the umbrella policy.

Importance of Integrating Umbrella Insurance with Existing Coverage

Umbrella insurance should be integrated with your existing coverage, such as auto and homeowners insurance, to provide comprehensive protection. This integration ensures that there are no gaps in coverage and that all potential liabilities are addressed. Working with an insurance professional can help you coordinate your policies and select the right coverage levels.

Case Studies and Real-World Examples

Examples of How Umbrella Insurance Has Protected Individuals

To illustrate the importance of umbrella insurance, consider the following real-world examples:

- Auto Accident: A high-net-worth individual was involved in a car accident that resulted in multiple injuries. The damages exceeded the limits of their auto insurance policy, but their umbrella insurance covered the additional costs, protecting their personal assets from being used to pay the settlement.

- Property Liability: A landlord faced a lawsuit after a tenant was injured on their rental property. The tenant's medical bills and legal fees surpassed the landlord's homeowners insurance limits, but the umbrella policy provided the additional coverage needed to settle the case.

- Defamation Lawsuit: A business owner was sued for defamation by a competitor. The legal fees and potential damages were substantial, but the umbrella insurance policy covered these costs, allowing the business owner to avoid financial ruin.

Analysis of Scenarios Where Lack of Umbrella Insurance Led to Significant Financial Loss

Conversely, there are numerous cases where individuals who lacked umbrella insurance faced devastating financial losses. For example, in cases of severe auto accidents or major property damage, the costs can easily exceed the limits of standard insurance policies. Without umbrella insurance, individuals may be forced to liquidate assets, sell property, or even declare bankruptcy to cover the costs.

The Future of Umbrella Insurance in the U.S.

Predictions on How Economic Trends Might Influence Demand for Umbrella Insurance

As economic trends continue to evolve, the demand for umbrella insurance is likely to increase. Rising medical costs, higher property values, and the growing complexity of legal cases all contribute to the need for additional liability coverage. Furthermore, as more individuals become aware of the risks associated with underinsurance, the adoption of umbrella policies is expected to rise.

The Potential Impact of Legal Reforms on Liability and Insurance

Legal reforms, particularly those aimed at reducing frivolous lawsuits or capping damages, could impact the liability landscape in the U.S. However, even with such reforms, the need for umbrella insurance is expected to remain strong, as the potential for significant financial losses due to liability claims will continue to be a concern for individuals and businesses alike.

Conclusion

In conclusion, umbrella insurance is a vital component of a comprehensive risk management strategy, especially in the current U.S. economic environment. It offers protection beyond the limits of standard policies, covering a wide range of liability risks that could otherwise lead to financial devastation. For individuals with substantial assets, high-risk occupations, or multiple properties, umbrella insurance provides peace of mind and financial security. As economic uncertainty persists, the importance of protecting oneself from unforeseen liabilities cannot be overstated, and umbrella insurance is an effective way to achieve this protection.

You May Also Like: